A- | A | A+ हिंदी

A- | A | A+ हिंदी

Skip to main content

A- | A | A+ हिंदी

A- | A | A+ हिंदी

Skip to main content

राष्ट्रीय Parishad of India

India’s Insurance industry is one of the premium sectors experiencing upward growth. This upward growth of the insurance industry can be attributed to growing incomes and increasing awareness in the industry. India is the fifth largest life insurance market in the world's emerging insurance markets, growing at a rate of 32-34% each year. In recent years the industry has been experiencing fierce competition among its peers which has led to new and innovative products within the industry. Foreign Direct Investment (FDI) in the industry under the automatic method is allowed up to 26% and licensing of the industry is monitored by the insurance regulator the Insurance Regulatory and Development Authority of India (IRDAI).

The insurance industry of India has 57 insurance companies - 24 are in the life insurance business, while 34 are non-life insurers. Among the life insurers, Life Insurance Corporation (LIC) is the sole public sector company. There are six public sector insurers in the non-life insurance segment. In addition to these, there is a sole national re-insurer, namely General Insurance Corporation of India (GIC Re). Other stakeholders in the Indian Insurance market include agents (individual and corporate), brokers, surveyors and third-party administrators servicing health insurance claims.

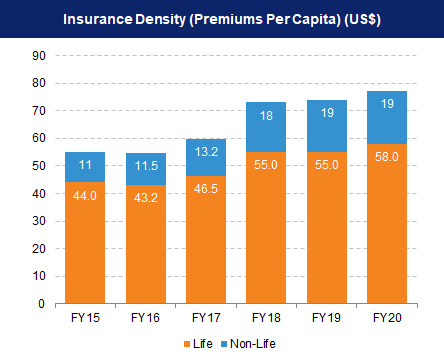

The insurance industry in India has witnessed an impressive growth rate over the last two decades driven by the greater private sector participation and an improvement in distribution capabilities, along with substantial improvements in operational efficiencies.

The premium in the month of March 2023 for the private life insurance industry grew at a healthy pace of 35% on a year-on-year basis and 20% for FY23.

Life insurance firms collected 18% more premiums in FY23 compared to the year before. Life insurers collected Rs. 3.71 lakh crore (US$ 44.85 billion) as the first-year premium in FY23 as against Rs. 3.14 lakh crore (US$ 37.96 billion) in FY22, shows the latest IRDAI data.

As expected, the state-run insurance behemoth LIC alone contributed over 60% to the total new business premium collection. The insurer received close to Rs. 2.31 lakh crore (US$ 27.93 billion) as premium in FY23 compared to Rs. 1.99 lakh crore (US$ 24.06 billion) in FY22.

The following are some of the major investments and developments in the Indian insurance sector.

The future looks promising for the life insurance industry with several changes in the regulatory framework which will lead to further changes in the way the industry conducts its business and engages with its customers. Life insurance industry in the country is expected to increase by 14-15% annually for the next three to five years. The scope of IoT in Indian insurance market continues to go beyond telematics and customer risk assessment. Currently, there are 110+ InsurTech start-ups operating in India. These startups are expected to provide a major boost to the industry and help increase India’s insurance penetration which plays a crucial role in the overall development of the country. In the past, the Indian government has played a crucial role in increasing the scope of the insurance sector through various policies and schemes. This trend will continue in the further through schemes like the Pradhan Mantri Fasal Bima Yojana (PMFBY) providing crop insurance and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) providing life insurance coverage to the youth at an affordable price. Schemes like these coupled with India’s demographic factors such as a growing middle class, young insurable population and growing awareness of the need for protection and retirement planning will support the growth of the Indian insurance sector.